2016-02-29. Why devaluation is the wrong medicine for the Greek economy

German Finance Minister Wolfgang Schäuble, at an event in Hamburg recently, referred to the proposal he had made to former Finance Minister Evangelos Venizelos in 2011 for Greece to temporarily exit the euro. Mr. Schäuble’s reasoning, and more, is that exiting the euro would allow the country to devalue its currency. The devaluation would hit the Greek economy once and for all, avoiding the “endless process” of harsh measures.

Behind this seemingly logical argument lies the following bitter truth: currency devaluations help an economy return to growth and employment growth, but with conditions that, unfortunately, Greece does not have. And if it wants to obtain them, the fiscal “pain” will be the same, or even worse, than that of the memoranda. The difference is now that the economy is a member of a strong and internationalized currency. Whereas with the drachma, Greeks would have to pay something more in the form of austerity measures to gain the credibility of the new currency in the long run.

However, from the constant resurgence of the drachma issue for at least five years, it appears that the theoretical arguments do not seem convincing enough.

So let's see what the numbers say and what the harsh reality has shown in three cases: Greece, Britain and Indonesia. In Britain, the devaluation of the 1990s succeeded because as an economy it was export-oriented. In Indonesia, in the same decade, the devaluation turned into a deep 14% recession and high inflation. Because it failed to increase its exports.

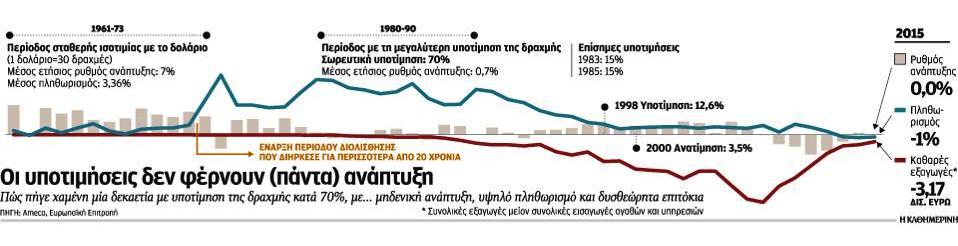

Let's stay in Greece. A look back at the drachma over the last 50-60 years leads to the following conclusions:

First, from 1954 to 1973, when the drachma had stabilized at 30 drachmas to 1 dollar, an average annual growth rate of around 17% was achieved.

Secondly, from 1974 onwards, a gradual slide of the drachma began, which peaked in the 1980s and lasted for at least 15 years. During this period, the drachma was devalued by 70%, while the annual growth rate was around zero! Also, despite the cumulative devaluation by 70% from 1980 to 1990 and despite the two official devaluations by 15% in 1983 and an additional 15% in 1985, net exports decreased and the trade deficit increased. In other words, competitiveness declined. During the same period, inflation reached levels of 25% and interest rates at 35%, essentially freezing all economic activity.

Third, the 1983% devaluation of 15 was accompanied by a 1,1% recession that year.

Fourth, the 1985% devaluation of 15 brought growth of 2,5% that year and just 0,5% in 1986, only for recession to return (-2,3%) in 1987.

Somehow the decade of 1980-1990 was lost with two devaluations and zero growth. Thus, stabilization (austerity) programs were needed at that time, which were proposed by the then Minister of National Economy, Costas Simitis. Necessary for the stabilization of the economy, after the official devaluations in 1983 and 1985.

Fifth, since 1998 and as the country prepares for the euro, the behavior of the economy has been changing. The 1998% devaluation of 12,6 did not bring about a recession. Nor did the 3,5% appreciation of the drachma in 2000 (in view of the euro) bring about a recession. On the contrary, the link between the drachma and the "strong" euro brought about, for at least a decade, growth at annual rates of around 3,5% and inflation below 3%.

The harsh reality, then, and economic theory says that devaluing a currency can help as long as the country does not import more than it exports and especially does not import many raw materials or intermediate materials for processing. If a country has these characteristics and decides to devalue, then it will sink… into recession and be “baked” by inflation.

This happens because the wrong medicine is given to the wrong disease. The devaluation of a currency aims to make exports cheaper. The increase in exports will lead to increased production and this in turn to increased employment. This entire chain leads to increased economic activity, through investment, higher consumption and incomes.

What can go wrong in this chain? If a country "doesn't produce" and imports more than it exports, then devaluation makes imports more expensive. If, for example, a textile industry imports fibers and dyes to export finished yarns, devaluation will not make it more competitive. It will close it down. The fibers and dyes will become very expensive.

In a country, therefore, with a negative trade balance, which imports many raw materials, devaluation increases production costs and creates inflation. The increase in production costs "eliminates" part of the competitiveness that was secured by devaluation. If inflation now passes through to wages, then all the profit from devaluation has been lost. Because, in the end, nothing has become cheaper.

Harsh austerity measures are the only way out

For a devaluation to succeed in a country like ours, it would have to:

First, there should be no wage increases. Nominal reductions may also be necessary. Therefore, the inflation rate would at best be the reduction in real incomes.

Secondly, changing the economic model, i.e. the country from an import-based to an export-based one. Something that does not happen overnight, and along the way there would be lockouts and many changes in labor (liberalization of markets, services, etc.).

Third, because borrowing would become more expensive, the budget would have to be as balanced as possible. That is, no deficits. Therefore, tax increases and spending cuts would be necessary. Because the drachma and its devaluation can solve the issue of competitiveness (and growth) under certain conditions, but not the problem of financing. In fact, if you "cut" new money, then this will become inflation and automatically its percentage will have to be converted into... cuts in wages and pensions. Otherwise, if increases are made, then new money will have to be "cut again", inflation will increase again and in order to make the economy cheaper, a new devaluation will have to be made... In other words, a vicious circle, which will be closed either with bankruptcy or with harsh austerity measures.

In other words, memorandum measures and their strict implementation would be needed, without the…memorandum money. Besides, even now, "internal devaluation" is taking place, that is, within the euro.

REPUBLISHED from Kathimerini, Sunday, 28/2/2016